Summary

Following the Arab Spring, Egypt and Tunisia are undergoing very difficult economic situations that risk affecting the economic viability of their political transitions. Meanwhile, both Morocco and Algeria have experienced rioting and there is growing uncertainty as to how economic policies might evolve in the future. This is especially so in Morocco, where tough economic decisions are almost as urgent as in Tunisia and Egypt. Libya faces the distinct challenge of managing its resource wealth from a ground-zero institutional setting. Mauritania is following a different political economy path and will therefore not be analysed here. From the point of view of political economy, a crucial point is whether the wave of popular revolts that overthrew the incumbent regimes will consolidate into economically-viable liberal democracies, and in what economic direction Algeria and Morocco will move, since to date they have been spared regime changes with a high budgetary cost. In other words, the question is whether democratisation can be maintained (or continue to be pursued) under current political economy conditions –meaning by that the full array of economic structures, institutions, interests and preferences of the various players in society–.

Introduction

The classic modernisation argument on the political economy preconditions for democratization sets a clear agenda: attaining an economic development threshold, education, the emergence of a middle class, the decentralization of economic power, a Weberian bureaucracy and Schumpeterian entrepreneurs, among others (Lipset, 1959, 1994; Rostow, 1960). To this process, economic demography added the modernization impact of demographic transition (Bloom et al., 2003), and economic institutionalism a set of basic economic institutions (North, 1990). While such a modernization agenda has been largely discredited in the Arab World, perhaps in perspective it might prove to have been not so wrong after all. It explains quite well what actually happened in Tunisia –the ‘Tunisian Paradox’ (Martinez, 2011)–: the more modern socio-economic ecosystem is the first to revolt. This does not imply supporting a sequencing approach in the sense of waiting for all the elements to be in place, checking modernization ticks in a pre-determined chronological order to reach the final stages and qualifying for democratisation (Carothers, 2007). Political transitions are seldom ordered, gradual and sequenced, nor suited to a one-fits-all model. For instance, the propensity to revolt tends to increase when the opportunity cost of revolting is low, which makes countries with high inequality or low economic opportunities more prone to revolutions (Acemoglu & Robinson, 2001).

In any case, it might be useful to remember the usual set of political economy pre-conditions for democratization in order to gain some insight into its long-term viability in North Africa. Admittedly more sophisticated versions of them have been used in the wake of the Arab Spring to try to explain (although ex-post) the economic causes of the revolts that overthrew the Egyptian, Libyan and Tunisian dictatorships and seriously challenged the Algerian and Moroccan regimes. Recent analyses point to education coupled with low employment opportunities (Campante & Chor, 2012), the birth of the individual due to demographic transition (Fargues, 2012), inherited institutional deficits (Chaney, 2012), the expansion of entrepreneurship and the private sector (Escribano & Lorca, 2012), and the overall unsustainability of the state (Colombo & Tocci, 2011).

The present chapter argues that changing political economy balances have been a significant driver for transformation, and that they remain a key factor in the future economic viability of democratisation. The following chapter starts by presenting the evolution of the North African countries’ economic situation and policies, and a brief assessment on the economic impact of the Arab Spring. It then analyses the different players, old and new, in a rapidly changing economic and political arena, highlighting the impact of modernisation and diversification in the emergence of a middle class which is not necessarily modelled on Western bourgeoisie. The chapter concludes with a warning against the temptation of addressing legitimate social justice demands through short-term populist economic policies instead of building a consensus for more inclusive patterns of growth.

The economy

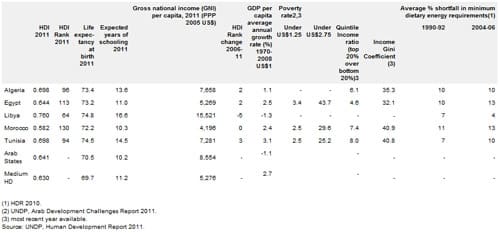

As shown in Table 1, the North African countries have attained a medium level of economic development, ranking in the high to medium segment in the 2011 Human Development Index (HDI): Libya is 64th, Tunisia 94th, Algeria 96th, Egypt 113th, and Morocco 130th. All the components of the HDI have improved in the region, which is now above the average medium human development and Arab State figures, with the sole exception of Morocco. Life expectancy has greatly increased over the last decades, and the region benefits from higher figures than the average for both Medium Human Development countries and Arab States. Schooling has also progressed, but there are significant differences across the region, with Algeria, Libya and Tunisia well above the average expected years of schooling of Arab States and Medium Human Development countries. Morocco and Egypt, on the contrary, are at the average of both country groups.

The dispersion of HDI levels is due to significant differences between countries in education, health and income per capita, with Libya benefiting from its hydrocarbon revenues and a relatively small population. Table 1 shows how income per capita ranges from over US$15,000 (2005 PPP) in Libya to almost US$4,200 in Morocco and US$5,300 in Egypt. Algeria and Tunisia are in between, at over US$7,000. GDP per capita growth has been much higher in resource-poor than in resource-rich countries, with Libya even reducing it in the last 30 years in line with the aggregate figures for Arab States; Algeria also shows a disappointing per capita growth figure. On the contrary, Egypt, Morocco and especially Tunisia registered significant GDP per capita growth figures, similar to those of Medium Human Development country averages.

Table 1. Human Development Indicators

Click to enlarge image

After the 2011 revolts, several analyses identified poverty, inequality and even food scarcity as drivers of popular discontent. While human development rapidly increased during the last two decades, the pace of improvement slowed down in the second half of the past decade, when only Algeria, Egypt and Tunisia modestly scaled up the HDI rank. Notwithstanding the region’s harsh economic and social realities, a more careful analysis shows the need to qualify such arguments. Income inequality is not extreme: Algeria has a Gini coefficient similar to Spain, Morocco and Tunisia to the US, and Egypt to Canada. These are lower figures than for emerging countries like Brazil (53.9), Russia (42.3) and China (41.5). The quintile income ratio is 8 in Tunisia and 7.4 in Morocco, figures comparable to those for the US and the UK. It is 6.1 for Algeria (a similar ratio to Spain and lower than Italy), and 4.6 in Egypt (comparable to Germany’s 4.3). Nuancing the extent of inequality is important because highly unequal societies are less likely to see their democracies consolidated (Acemoglu & Robinson, 2001).

The region also has lower than expected poverty levels considering its income level. The poverty rate for population under the US$1.25 poverty line is 3.4% in Egypt and 2.5% in Morocco and Tunisia. These rates compare well with poverty rates in other emerging countries like Brazil (3.8%), Mexico (3.4%), China (16.2%) and India (41.6%). When the poverty line is raised to US$2.75, poverty rates increase steadily to 43.7% in Egypt, 29.6% in Morocco and 25.2% in Tunisia. These figures do not compare so well with those for Brazil (16.4%) and Mexico (14.4%), but are far below China (53.8%) and India (88.6%). They are also below average poverty rates for the developing world (23.6% under the US$1.25 line and 60.5% under the US$2.75 threshold), and somewhat lower than for Arab countries as a whole, where they reach 3.9% and 40.0%, respectively. In both cases the region has experienced a significant decrease in poverty rates, with the sole exception of Morocco for under US$1.25 rate, which stagnated between 1991 and 2007. Poverty is mainly a rural phenomenon, but there are also some peri-urban poverty bags that tend to be more visible.

While ‘bread revolts’ due to food subsidy reductions have been common in the past and one of the components of recent demonstrations, it does not seem from nutritional data that access to food is a significant problem for these countries, with average shortfalls similar to those in Poland and Romania. However, the trend differs between countries, with Egypt, Morocco and Tunisia experiencing a clear deterioration in their nutritional figures. Algeria has stagnating figures and only Libya registered a decrease in malnutrition data. This picture may not make justice to the significant number of people that are still suffering from deprivation in North Africa, but it points to the fact that the socio-economic situation alone probably cannot account for the revolts of 2011. In fact, they have been more violent in Libya, the richer country, and most successful in Tunisia, which comes second in the North African HDI rank.

It has been argued that North African figures on poverty and inequality are underestimated, and that they do not reflect the socio-economic penuries afflicting the region (UNDP, 2011b). While there is evidence that such a problem with North African statistical figures may exist, accounting for it does not significantly change the picture, as recognised by its proponents: compared to most other developing regions North Africa suffers from low levels of poverty. However, it is equally true that in the recent past progress in reducing poverty has been amongst the slowest across regions and cannot be expected to significantly reduce poverty in the coming future (UNDP, 2011b, p. 24). A more sophisticated argument regarding the economic causes of the Arab revolts is precisely that modernization and social transformation outpaced the North African regimes’ capacity to deliver on socio-economic demands. In other words, the economic legitimacy of autocracy was increasingly challenged by broader and more demanding middle classes: the cost of autocracy simply no longer compensated for the meagre economic benefits delivered by North African governments.

Regarding macroeconomic figures, stability and macro-prudency (with the eternal Libyan exception) over the last two decades have stabilized North African economies and provide the basis for sustained growth in the last decade and increased resilience to external shocks. As shown in Table 2, during the 2000s economic growth has stabilized after decades of volatility and even in the midst of the crisis remained at relatively high levels. While growth in Algeria and especially Libya remained strongly dependent upon hydrocarbon prices, Morocco and Tunisia have seemingly achieved a more sustained growth path. Inflation also remained under control, but at the cost of repressing prices through food and energy subsidies. To a great extent Algeria, and to a lesser extent Libya, succeeded in sterilizing huge hydrocarbon revenues and the macroeconomic mismanagement that led to past Dutch Disease episodes did not materialize. Morocco and Tunisia have lower inflation records, but their vulnerability to energy and food international prices in 2008 may be seen in Table 2.

Table 2. Selected Macroeconomic Indicators

| Real GDP Growth (%) | |||||||

| Average 2000-05 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 (1) | |

| Algeria | 4.5 | 3.0 | 2.4 | 2.4 | 3.3 | 3.9 | 2.6 |

| Egypt | 4.4 | 7.1 | 7.2 | 4.7 | 5.1 | 1.8 | 2.0 |

| Libya | 4.3 | 6.4 | 2.4 | -1.4 | 3.7 | -59.7 | 121.9 |

| Morocco | 4.4 | 2.7 | 5.6 | 4.9 | 3.7 | 4.9 | 2.9 |

| Tunisia | 4.4 | 6.3 | 4.5 | 3.1 | 3.1 | -1.8 | 2.7 |

| Consumer Price Inflation (%) | |||||||

| Algeria | 2.3 | 3.6 | 4.9 | 5.7 | 3.9 | 4.5 | 8.4 |

| Egypt | 5.1 | 9.5 | 18.3 | 11.7 | 11.4 | 9.9 | 9.7 |

| Libya | -3.3 | 6.2 | 10.4 | 2.4 | 2.5 | 5.6 | 6.0 |

| Morocco | 1.5 | 2.0 | 3.9 | 1.0 | 1.0 | 0.9 | 2.2 |

| Tunisia | 2.7 | 3.4 | 4.9 | 3.5 | 4.4 | 3.5 | 5.0 |

| Government Fiscal Balance (% GDP) | |||||||

| Algeria | 6.6 | 4.4 | 7.6 | -6.4 | -2.3 | -0.2 | -3.9 |

| Egypt | -6.8 | -7.5 | -8.0 | -6.8 | -7.8 | -9.9 | -11.1 |

| Libya | 12.6 | 24.0 | 25.1 | -3.0 | 16.7 | -27.7 | 19.4 |

| Morocco | -5.2 | -0.1 | 0.7 | -1.8 | -4.4 | -6.9 | -6.1 |

| Tunisia | -2.6 | -2.8 | -0.7 | -2.6 | -0.9 | -3.1 | -6.4 |

| Current Account Balance (% GDP) | |||||||

| Algeria | 14.0 | 22.8 | 20.1 | 0.3 | 7.5 | 10.0 | 6.2 |

| Egypt | 1.6 | 1.7 | 0.5 | -2.3 | -2.0 | -2.6 | -3.4 |

| Libya | 18.9 | 43.8 | 42.3 | 14.7 | 19.8 | 1.3 | 21.8 |

| Morocco | 2.2 | -0.1 | -5.2 | -5.4 | -4.3 | -8.0 | -7.9 |

| Tunisia | -3.0 | -2.4 | -3.8 | -2.8 | -4.8 | -7.3 | -7.9 |

(1) Projections.

Source: IMF, Regional Economic Outlook, Middle East and Central Asia, October 2010 and 2012.

Fiscal balances also improved during the 2000s compared with past huge deficits and external debts. However, the fiscal balances of Morocco and Tunisia remained fragile and the fiscal policy space was limited and proved to be vulnerable to external shocks. Algeria has more fiscal space due to the cancellation of most of its external debt and to its high level of reserves, but remains vulnerable to oil prices (to which gas prices are indexed), showing that a share of fiscal revenues is illusory, while growing current expenses are not. The external balance started to deteriorate in the second half of the 2000s partly due to external shocks such as increases in oil and food prices. Significant current account surpluses in Egypt and Morocco turned into deficits in the second half of the 2000s and became increasingly subject to stress in both countries. Resource-rich countries experienced a reduction in their current account surplus. In Algeria the high surpluses of the recent past have been greatly reduced due to lower oil prices and reduced gas exports. The World Bank (2010) estimates that the change in the import bill due to a 50% increase in wheat prices accounts for as much as 0.4% of GDP for Morocco, Tunisia and Algeria. Libya has traditionally maintained a comfortable fiscal and external position built on hydrocarbon revenues and foreign exchange reserves.

But this overall positive outlook changed dramatically with the Arab Spring, which added to the already slowing economic growth due to the international financial crisis and the Euro crisis. As shown in Table 2, in 2011 growth rates diminished the most in the countries experiencing regime change. Egypt recorded a meager growth rate of 1.8% in 2011 compared with 5.1% in 2010, and IMF projections were not much more optimistic for 2012. In 2011 Tunisia registered its first year of recession for the last two decades, with GDP decreasing 1.8% and gloomy prospects for 2012. Strikes and other disruptions in economic activity seriously affected growth and exports, and the collapse of foreign sources of income, like tourism and investment, deepened the economic cost of the revolts. The Libyan disruption of oil production and exports caused the country’s growth rate to decrease by almost 60% in 2011, but its fast recovery is expected to boost GDP growth in 2012.

Morocco was also affected through deteriorating external inflows, mainly tourism and foreign investment, and rising uncertainty on the domestic political repercussions of the events in Tunisia and Egypt. But the country weathered the tension in 2011 quite well, achieving 4.9% GDP growth in 2011 due to fiscal countercyclical measures and a rainy agricultural season. Political uncertainty was reduced with a new government led by the Parti de la Justice et le Développement-PJD, committed to economic orthodoxy termed as ‘pragmatism’. But sluggish demand in Europe and a more prudent fiscal stance was expected to reduce GDP growth for 2012 to below 3%. In Algeria growth continued to be dependent on hydrocarbon prices and production.

The impact of the crisis has also been reflected by worsening macroeconomic balances. Fiscal income fell while expenses were fostered by the attempts to prevent both social unrest and the deepening of the economic downturn. Rising subsidies, public wages and public jobs translated into growing fiscal deficits in Egypt, Morocco and Tunisia for 2011 and 2012. Algeria also adopted a more pro-active fiscal policy that deteriorated its fiscal balance in 2012, but maintained a far greater fiscal policy space than its neighbors, with the only exception of Libya, whose huge fiscal deficit in 2011 was rapidly reverted to an almost 20% surplus in 2012. In spite of weak demand conditions and price repression, inflation remained at relatively high levels in Egypt and, to a lesser extent, Tunisia.

In Morocco inflation has been kept under control, but the easing of price repression (reduction of fuel subsidies) and fiscal deficit pressures is projected to double inflation in 2012. In Algeria, fiscal expansion and a less restrictive stance towards the sterilization of hydrocarbon income is expected to double inflation in 2012. The Egyptian, Moroccan and Tunisian external balances have also experienced a marked deterioration during 2001 and 2012. The most pressing situation is the Tunisian and Egyptian lack of foreign reserves, accounting at the end of 2012 for barely three months of imports; Morocco is also under pressure, with reserves for around six months of imports. Algeria enjoys a comfortable current account surplus, as does Libya after recovering from the 2011 oil export disruption.

North African economic policies have been criticized on the grounds that structural reforms, including institutional ones, have lagged behind macroeconomic stabilization (Escribano & Lorca, 2008). Some microeconomic and institutional reforms have been carried out during the past decades, but implementation has been slow, fragmented and sometimes inconsistent. Trade liberalization, reduction of domestic entry barriers, privatization and the upgrading of the business environment, among other measures, resulted in the diversification of economic activities, an increase in private-sector dynamism and a more open economic system. In the wake of the 2001 revolts, several reforms that awaited their turn for years, such as subsidy and fiscal reform, seemed to be on track. But one of the main (intangible) results of the Arab Spring is the discrediting of the overthrown regimes’ economic policies, including much needed microeconomic and institutional reforms. In this context, the economic evolution of North African countries remains uncertain. Before addressing its reconfiguration after the Arab Spring, the following section analyses the new political economy balances emerging across the region in order to try to capture their influence in the process of economic policy formulation.

A Shifting Political Economy Balance

The emergence of North African political economy balances is well documented in the region’s political economy literature. Colonial structures shaped regional and economic balances and, after independence, state-led growth and import substituting strategies generated an extractive class of public company managers and rent-seeking entrepreneurs (Richards & Waterbury, 2007). The model collapsed for the first time in the external debt crisis of the 1980’s. The stabilization and liberalization policies that followed remained subject to the economic elite’s preferences, which thanks to its political connections captured a large share of the rents derived from the reforms, including privatizations, public works and services contracts, trade liberalization, etc (Heydemann, 2004). This changed the rent-seeking model but basically let corporatist capitalism, together with privilege and cronyism, be the main entry barrier into the political economy space. The North African political economy has traditionally been based on the incumbents’ political networks of influence, exploiting economic reforms and renewing rent-extractive strategies (Greenwood, 2008).

In Egypt and Tunisia, Mubarak and Ben Ali knitted well-known business architectures to extract rents from their countries (Anderson, 2011). A cable revealed by WikiLeaks showed that in 2006 the US ambassador to Tunisia reported that more than half of Tunisia’s commercial elites were personally related to Ben Ali through an extractive network known as ‘The Family’. In Egypt, the network was based on the business connections of Mubarak’s son Gamal, which was somehow competing with military economic interests. In Morocco, the Mazkhen constitutes a network of influence around the Palace’s economic preferences and interests, including a network of businessmen that transit from the public to the private sector (Catusse, 2006). In Libya, the Gaddafi family directly appropriated oil income and there were no comparable economic reforms as those implemented in other countries in the region. Libyan reforms remained limited to the opening of the hydrocarbons sector to foreign investment, leaving political economy balances unchanged (Bruce St John, 2008). As a result, the private business fabric remained weak, and the economy is still completely dominated by the control of oil resources. In Algeria rent-seeking strategies are also centered on the capture of hydrocarbon wealth by le Pouvoir, an opaque body of generals, politicians and politically-connected businessmen (Martinez, 2010).

For sure, there are significant cross-country differences in the political economy weight of other traditional actors, such as the military and trade unions (Catusse, 2006). The economic influence of the military is mostly restricted to Egypt, where they control around one-third of Egypt’s GDP and conduct important economic activities in strategic sectors such as the iron and steel industry, construction, tourism and agro-food, among others (Alissa, 2007). As a result, they oppose economic liberalization and private-sector growth because they threaten its economic power, a position that was highly influential in the Egyptian provisional government (Anderson, 2011). The Algerian military exert control over hydrocarbon resources, opposing any effort to further open the sector to foreign investment, fearing it will weaken its political pre-eminence (Martínez, 2010). Trade unions are a powerful actor in Tunisia, as shown before, during and after the removal of Ben Ali, although their influence is much lower elsewhere in the region.

Even if slow and sometimes reluctant, economic reforms have slightly shifted the political economy equilibrium in favur of new actors, like small and medium enterprises (SMEs), foreign companies and professionals. Social change has also empowered other actors, like the youth, Islamist political parties, and women. Both economic and social transformation offer opportunities to forge new alliances between new actors, or between new and traditional ones. For instance, diversification and export orientation have created a new class of entrepreneurs integrated in transnational industrial networks, which coexist with a more traditional class of small and very small merchants and traditional services providers. While both groups differ in their approach, they share similar concerns regarding economic policy preferences. The economic elites may decide to accompany the emerging middle class and start to get rid of regime compliance costs when they start to exceed expected returns from rent-seeking.

A growing component of the middle class are liberal professionals, that when underemployed add to the ‘middle class’ poor. Another emerging economic actor is the informal sector, which accounts for a significant part of GDP and employment and is made out of a heterogeneous mix of micro-entrepreneurs in different sectors. Its role is ambiguous, acting as a driver of diversification and de-concentration of economic power, but at the same time reproducing traditional social mechanisms (Hibou, 2010). In this regard, the main influence that new entrepreneurs can have in promoting political change is the widening of a middle class with preferences different from those of the economic elites.

Big industrial firms dominate industry and older firms are disproportionally represented, showing they are able to survive any reforms. The age of local manufacturing firms in MENA averages 19 years, the same as mature OECD countries, and twice the figure in East Asia and Eastern Europe (World Bank, 2008). This makes the renewal of the industrial structure slower than elsewhere. The subsequent absence of renewal in the business elite, together with low mobility within companies, echoes what has been described by political scientists regarding political elites. However, within the region, firm creation has greatly increased in countries such as Morocco and Tunisia, while Algerian and especially Egyptian figures reflect very low firm renewal, reflecting differences in the degree of economic opening and business environment improvement. It also shows that when entry barriers are lowered, new economic actors enter the market, altering political economy balances (Escribano &Lorca, 2012). However, its impact has been limited by path-dependent institutional constraints (Kuran, 2010).

Foreign investors have had a mixed interests conflict with the ruling elites, they adopt exit strategies to optimize their investment returns. Foreign companies have certainly help to modernize the economic system, but have not significantly altered political economy balances. Multinationals in the Middle East tend to show a clear lack of commitment to the promotion of democracy (Youngs, 2011).

Youth is another new driver of change, especially in the economic realm. North Africa has a wide economic generation gap. As with politicians and high officials, businessmen tend to be older than in other developing regions (14 years of average experience compared with eight in Latin America and South Asia). This is especially frustrating in countries where youth account for a large proportion of the population. In addition, the level of education of the region’s businessmen is also lower (World Bank, 2008), explaining the widespread feeling of exclusion among better prepared young graduates that cannot access influential positions in either the public or private sectors.

The role of women in the public domain has also been slightly transformed, but their voice in economic issues remains marginal, as with young people. While men have somehow been able to capture part of the benefits of gender equality measures, this kind of gender-based rent-seeking is however increasingly challenged by businesswomen. They face additional entry barriers, but once these barriers are either relaxed or painfully surmounted they play a more significant transformative role in both the economic and political arenas than is the case for businessmen (Paciello & Pepicelli, 2012). Both youngsters and women asking for economic autonomy and a voice are powerful agents of change, but their influence risks being limited in a political context marked by the rise of religious conservatism, where the economic voice of young people tends to be subordinated to that of their elders and women’s to men’s.

This leads to the last of the new economic actors considered in this section, Islamist political parties and their domestic economic support base. Regarding its theoretical base, Islamic economics is so vague that almost any school of economic thought can find the way to defend its position on it. It is a normative corpus based upon a strong sense of social justice, which includes merit and protection of property rights. As in any other society, redistribution can be attained in different ways that are most usually explained by political economy balances rather than religious beliefs. In short, there is a political economy of Islamism which entails its own internal actors and balances.

The transformative role of Islamic Economics and its business dimension is ambivalent. The promotion of honesty, transparency and business success as self-accomplishment constitutes a vigorous driver for change. But other preferences can led to unrealistic social demands which pursue social justice by means of unsustainable populist policies. This can cause fiscal volatility and difficulties in consolidating democracy (Acemoglu & Robinson, 2001). Some authors have argued that Islamist policies can consist of a combination of economic liberalism with social conservatism (Roy, 2012). Such a mix offers uncertain results if social conservatism harms tourism, foreign investment or trade. It has been argued, from an economic institutionalist perspective, that popular support for Islamist groups can undermine democratic efforts by concentrating political power in their hands in the absence of checks on their power from other interest groups, such as labor unions and business interests (Chaney, 2012).

This appraisal disregards the fact that Islamists themselves have commercial interests, and underscores the entrepreneurial dimension of Islam. Islamic entrepreneurs have their own Schumpeterian attributes within a set of values influenced by Islam rather than Protestantism (Adas, 2006). They have grown considerably over the last decades, especially in Turkey, but also in some North African countries. They may turn out to be the most effective barrier to populist economic policies and the best positioned to balance the trade-offs between religious values and a functioning market economy. They are also the main source of local financing for Islamist movements, potentially reinforcing their influence in economic policy making. With all these elements in mind, the final section tries to offer some prospects for economic policy-making in the region over the coming years.

Economic Policy Prospects

The previous chapter has tried to show that the economic impact of the revolts has been significant. But the main question now is for how long its negative economic effects will last. Uncertainty has deeply affected economic activity: Tunisia and Egypt have lost more than half of their tourism revenues; foreign investment, which was already low due to the international crisis, has simply halted; government packages to increase wages and subsidies have already been implemented at a high fiscal cost. Other impacts have been more short-lived, like logistical chain disruptions in Tunisian and Egyptian industrial international networks, oil and gas supply disruptions in Libya, capital flights or the decrease of remittances in Tunisia and Egypt. But on the whole, short-term economic prospects for the region look rather gloomy. Coping with increasing social pressures to raise social expenses and mounting political uncertainty in a context of macroeconomic fragility and international crisis is not going to be easy. This is especially so for non-oil exporters, but in the long term also for Algeria. In Libya, the economic evolution would depend on the governance of oil and gas production and exports. Both countries face the distinct challenge of escaping both Dutch Disease and Resource Curse in a more demanding political context.

After the Arab Spring, all North African (and most Arab) countries increased public wages and employment, food and energy subsidies, and public works. These measures have been presented as a commitment to advance social justice and to signal that policies have changed towards a more inclusive pattern of redistribution and growth. Plausible political economy scenarios are however not uniform across the region, because countries’ trajectories widely differ. Libyan and Algerian political economy balances are determined by a huge and highly centralized hydrocarbon rent, and consequently by a lower degree of diversification and influence of private actors. In principle, oil and gas rents raise their regimes’ propensity to fierce political economy bargaining and are therefore more conflict-prone. Algeria is far more diversified than Libya and is much more advanced in economic reforms. But even rentier economies able to provide stability through broader redistribution measures have developed an unsustainable political economy balance which will press for the inclusiveness of new societal actors (Ross et al., 2011). Tunisia and Morocco have attained a higher level of diversification and middle class autonomy from the State, with rents being transferred in a manner that is more diffuse and difficult to capture. They also count on relatively better management skills, both public and private. Tunisia and Libya are relatively small countries, while Morocco and Algeria host significant populations and have a greater geopolitical and geo-economic role to play. But, although to a different extent, all of them are still facing the challenge of state sustainability (Colombo, 2011; Paciello, 2011).

From a political economy perspective, the main contribution of past economic reforms to political change has been facilitating social mobility and diversifying economic power by expanding the middle class and slowly renewing economic and business elites. This has helped to alter the political economy balances within societies by favoring the decentralization of economic power away from big entrepreneurs and public companies that tend to support the regimes in place. This gradually eroded the elites’ capacity to exert social control through patronage and nepotism, lowering the opportunity cost of revolting. However, the region’s institutional framework is clearly deficient, with high levels of corruption and low efficiency in public and private management. Entry and exit in private and social activities is difficult and costly, limiting social mobility and lowering the pace of elite renewal. Institutional and microeconomic reforms remain a key factor in opening the economic policy space while reducing its volatility.

Finally, perhaps the most pressing obstacle relates to short-term economic challenges, which may prove to be politically very costly. This includes rationalizing food and energy subsidies by implementing social targeting, continuing external liberalization, maintaining a prudent macroeconomic stance and resisting fiscally unsustainable –however socially praiseworthy– political demands. Some Islamist-led governments, like Morocco’s, have advanced in this domain, containing the fiscal deficit and rationalizing fossil fuel and electricity subsidies. This proves that, within Islamist parties, pragmatism can overrule populism, greatly contributing to the viability of democratic transitions. Islamists are aware that they have to deliver on the economic domain, but also that their results cannot be short-lived. They also know that part of their constituency, such as the pious middle class, watch their economic interests closely and will not tolerate a damaging populist stance.

However, the populist scenario remains a risk, especially if the legitimacy gained by elected governments starts to be eroded by conflict between internal actors. Economies in political transitions tend to be difficult to manage, all the more so during an international economic crisis. The region is exploring its economic options and realizing that its policy space is quite reduced. Islamic normative economics do not provide answers to the pressing problems of transition, and it is urgent for North African governments to present a credible and sustainable economic model to their constituencies. For sure, the mixed picture presented in this chapter does not reproduce the modernist ideal of a harmonious and diversified society, with innovative entrepreneurs being managed by Weberian-ethics bureaucrats, strong institutions that protect property rights and provide checks and balances against social dominance, and a wide educated middle class that has attained a homogeneous and secular life-style. Not all the elements are in place and perfectly aligned to offer the best transition model that guarantees stable democratization, and its combination certainly varies across countries. But it would be wise to let North African societies make their evolving political economy balances work in order to develop an economic model they can recognize as optimal according to their own preferences.

Gonzalo Escribano

Senior Analyst, Elcano Royal Institute of International Studies, and Professor of Applied Economics, Spanish Open University (UNED)

Bibliographical References

Acemoglu, D., & J.A. Robinson (2001), ‘A Theory of Political Transitions’, American Economic Review, vol. 91, nr 4, p. 938-963.

Adas, E.B. (2006), ‘The Making of Entrepreneurial Islam and the Islamic Spirit of Capitalism’, Journal for Cultural Research, vol. 10, nr 2.

Anderson, L. (2011), ‘Demystifying the Arab Spring. Parsing the Differences Between Tunisia, Egypt, and Libya’, Foreign Affairs, vol. 90, nr 3, pp. 2-7.

Bloom, D.E., D. Canning & J. Sevilla (2003), The Demographic Dividend: A New Perspective on the Economic Consequences of Population Change, RAND, Santa Monica, CA.

Campante, F.R., & D. Chor (2012), ‘Why was the Arab World Poised for Revolution? Schooling, Economic Opportunities, and the Arab Spring’, Journal of Economic Perspectives, nr 26, pp. 167-188.

Carothers, T. (2007), ‘How Democracies Emerge-The Sequencing Fallacy’, Journal of Democracy, vol. 18, nr 1.

Catusse, M. (2008), Le temps des entrepreneurs? Politique et transformations du capitalisme au Maroc, Maisonneuve et Larose, Paris.

Catusse, M. (2006), ‘Ordonner, classer, penser la société: Les pays arabes au prisme de l’économie politique’, in E. Picard (ed.), La Politique dans le Monde Arabe. A. Colin, Paris, pp. 215-238.

Chaney, E. (2012), ‘Democratic Change in the Arab World, Past and Present’, Brookings Papers on Economic Activity, vol. 42, nr 1, pp. 363-414.

Colombo, S. (2011), ‘Morocco at the Crossroads: Seizing the Window of Opportunity’, in Colombo and Tocci (Eds.), pp. 161-192.

Colombo, S., & N. Tocci (2011), The Challenges of State Sustainability in the Mediterranean. Nuova Cultura-Istituto Affari Internacionali, Rome.

Escribano, G., & Lorca, A. (2008), ‘Economic Reform in the Maghreb: From Stabilization to Modernization’, in Zoubir & Amirah-Fernández (Eds.), pp. 135-158.

Escribano, G., & A. Lorca (2012), ‘Modern Commercial and Social Entrepreneurship as a Factor of Change’, in Merlini & Roy (Eds.), pp. 96-122.

Fargues, P. (2012), ‘Demography, Migration, and Revolt in the Southern Mediterranean’, in Merlini & Roy (Eds.), pp. 17-46.

Greenwood, S. (2008), ‘Bad for Business? Entrepreneurs and Democracy in the Arab World’, Comparative Political Studies, vol. 41, nr 6, 837-860.

Heydemann, S. (Ed.) (2004), Networks of Privilege in the Middle East: The Politics of Economic Reform Revisited, Palgrave, London.

Hibou, B. (2010), ‘Discipline and Reform – I’, Sociétés politiques comparées, 22, February.

IMF (2012), Regional Economic Outlook, Middle East and Central Asia, October 2012. Washington DC.

IMF (2010), Regional Economic Outlook, Middle East and Central Asia, Washington DC, October.

Kuran, T. (2010), ‘The Scale of Entrepreneurship in Middle Eastern History: Inhibitive Roles of Islamic Institutions’, in W. Baumol, D. Landes & J. Mokyr (Eds.), The Invention of Enterprise: Entrepreneurship from Ancient Mesopotamia to Modern Times, Princeton University Press, Princeton & Oxford, pp. 62-87.

Lipset, S.M. (1959), ‘Some Social Requisites of Democracy’, American Political Science Review, vol. 53, nr 1.

Lipset, S.M. (1994), ‘The Social Requisites of Democracy Revisited’, American Sociological Review, vol. 59, nr 1.

Martínez, L. (2011), ‘La Leçon Tunisienne’, ISS Opinion, January.

Martínez, L. (2010), Violence de la rente pétrolière: Algérie, Irak, Libye, Presses de Sciences Po, Paris.

Merlini, C., & O. Roy (Eds.) (2012), Arab Society in Revolt: The West’s Mediterranean Challenge, Brookings Institution Press, Washington.

North, D.C. (1990), Institutions, Institutional Change and Economic Performance, Cambridge University Press, Cambridge, MA.

Paciello, M.C. (2011), ‘Egypt: Changes and Challenges of Political Transition’, in Colombo & Tocci (Eds.), pp. 101-160.

Paciello, M.C., & R. Pepicelli (2012), ‘The Changing Role of Women in Society’, in Merlini & Roy (Eds.), pp. 53-75.

Richards, A., & J. Waterbury (2007), A Political Economy of the Middle East, Westview Press, Boulder, Co., 3rd edition.

Ross, M., K. Kaiser & N. Mazaheri (2011), ‘The ‘Resource Curse’, in ‘MENA? Political Transitions, Resource Wealth, Economic Shocks, and Conflict Risk’ World Bank Policy Research Working Paper 5742, July.

Rostow, W.W. (1960), The Stages of Economic Growth: A Non-communist Manifesto, Cambridge University Press, Cambridge, MA.

Roy, O. (2012), ‘Islamic Revival and Democracy: The Case in Tunisia and Egypt’, in Merlini & Roy (Eds.), pp. 47-52.

St John, R. Bruce (2008), ‘Libya: Reforming the Economy, Not the Polity’, in Zoubir & Amirah-Fernández (Eds.), pp. 53-70.

UNDP (2011a), Human Development Report 2011, New York.

UNDP (2011b), Arab Development Challenges Report 2011. Towards the Developmental State in the Arab Region, Cairo.

UNDP (2010), Human Development Report 2010, New York.

World Bank (2010), Sustaining the Recovery in Times of Uncertainty, Middle East and North Africa Regional Economic Outlook, Washington DC.

Youngs, R. (2011), ‘Misunderstanding the Maladies of Liberal Democracy Promotion’, FRIDE working paper, nr 106, January.

Zoubir, Y., & H. Amirah-Fernández (Eds.) (2008), North Africa: Politics, Region, and the Limits of Transformation, Routledge, London.