Despite its small size, with a population of only 3.4 million, and its geographical location, sandwiched between two giants such as Brazil and Argentina, Uruguay frequently features in the international press.

These regular appearances are generally to highlight positive aspects regarding its solid institutions, its democratic credentials, its economic stability and predictability, its social protection network and its foreign policy, where Uruguay stands out as a good neighbour in the international community.

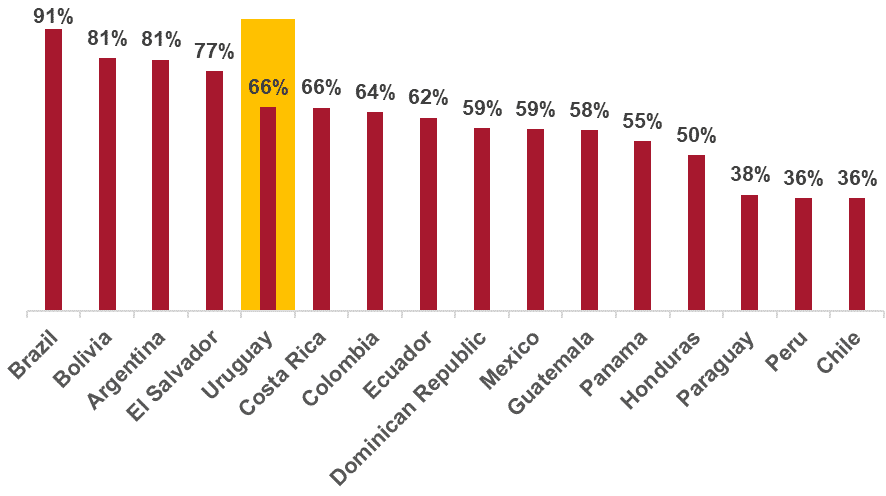

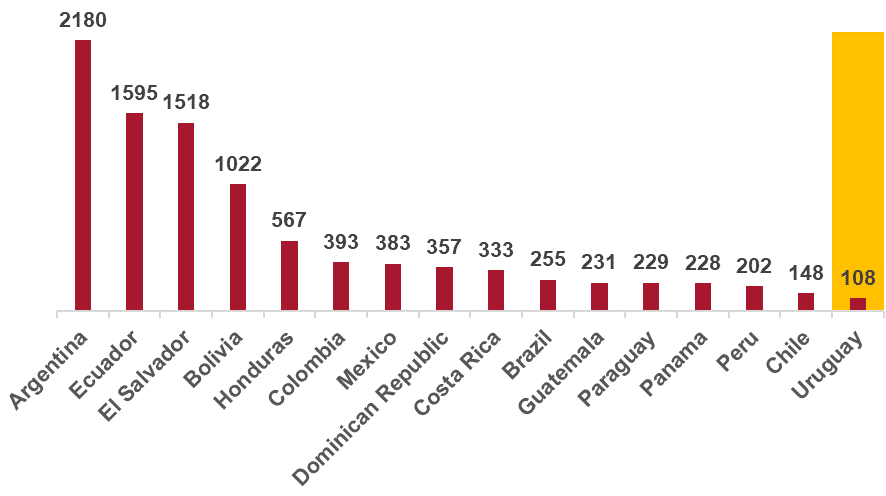

The most recent appearance poses a puzzle that has surprised many market analysts: Uruguay has one of the highest levels of public debt in Latin America –in the top third– and at the same time enjoys the lowest credit risk –as measured by EMBI spreads– in the region (see Figures 1 and 2).

Figure 1. Public debt in Latin America (% of GDP)

Figure 2. Credit risk in Latin America (EMBI Spread, average January-April 2023)

How can we explain this puzzle? The short answer is that Uruguay’s fiscal policy has been textbook optimal.

During the pandemic Uruguay created a COVID fund to finance exceptional outlays while simultaneously reducing the structural budget deficit in its regular public finance accounts.

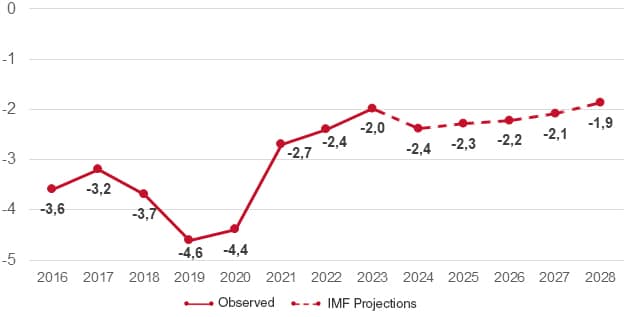

With levels of output slightly above and unemployment and inflation slightly below their 2019 pre COVID levels, the structural fiscal deficit in 2022 was around 2.4% of GDP, 2.2% of GDP below 2019, the year before the pandemic. Moreover, according to IMF projections the structural deficit is expected to reach the 2% level that stabilises public debt to GDP.

Figure 3. Uruguay’s structural fiscal balance (% of GDP, including Central Government and Social Security system)

Second, in the midst of the pandemic, Uruguay approved a law creating a new institutional framework for the management of its public finances. The law establishes a fiscal rule that aims to strengthen fiscal responsibility and sustainability and reduce procyclicality and discretionality in spending.

The fiscal rule establishes indicative targets and rests on three pillars: (a) a cap on the structural fiscal balance; (b) a cap on the yearly increase of real primary expenditures relative to potential GDP; and (c) a cap on indebtedness. Despite the adverse context since the enactment of the fiscal rule, the government managed to meet the spending target.

Third, and very importantly, Uruguay has just approved a Social Security reform that, beyond some of its positive or more questionable provisions about the system’s design, incentives and fairness, ensures long-term fiscal sustainability and credibility.

Social Security reform is a signal that the political system is willing and able to reach agreements to enact reforms that are politically costly, complex to negotiate and that have an impact that goes beyond the current administration and spans many governments.

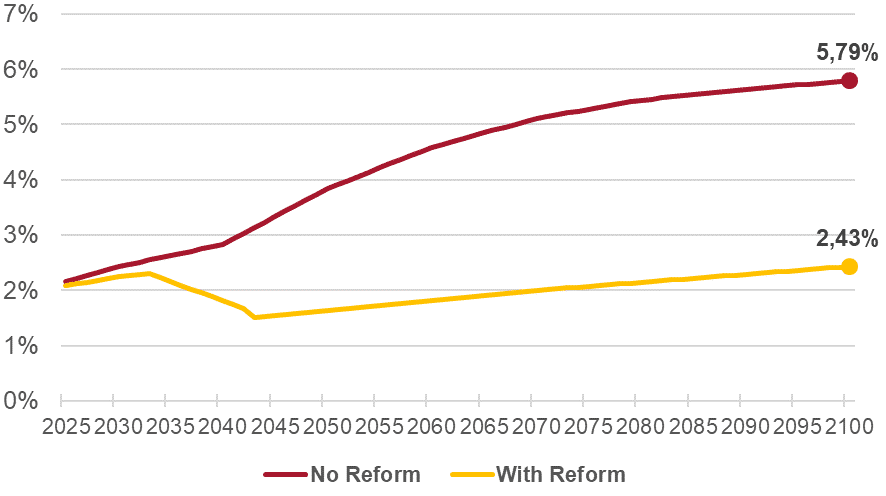

In addition, by reducing the annual deficit of the Social Security system, it reduces the implicit debt in the system’s unfunded liabilities by around 130% of GDP, double the observed public debt level.[1]

Figure 4. Deficit of Uruguay’s Social Security system (% of GDP)

The market’s recognition of these fiscal policy decisions, together with the fact that even with a change of government they are not expected to be reversed, means that Uruguay enjoys the region’s lowest credit risk, and for the first time in history its credit rating was upgraded by Standard & Poor’s to BBB+.[2] The moral of this story is that when policy decisions have an impact in the future, ‘what you don’t see is what you get’: in this case, the expected structural budget deficit, that stabilises growth of public debt, and Social Security reform, that reduces implicit public debt, while both leave observ

[1] A real discount rate of 3% per annum was used for the calculation. If the real discount rate were 4%, the implicit debt reduction would be 82% of GDP, and if it were 2%, it would be 200% of GDP. In all cases, this is a significant figure relative to observed public debt.

[2] Something similar happened with the 1996 social security reform. As a result of it, the system’s implicit debt was also significantly reduced and Uruguay obtained investment grade status for the first time.

Elcano Comments

This is a new initiative of the Institute that aims to offer analyses by experts on topics that are within the scope of our research agenda. They are published on no regular basis but as opportunity arises in accordance with the advice of the broader academic community in cooperation with the Elcano Royal Institute.