Theme[1]: The aim of this paper is to understand China’s strategic behaviour towards the European Monetary Union (EMU).

Summary: The first section of this paper chronologically summarises China’s support for the single currency since its creation up to the Eurozone crisis. The second section explains why China has been so supportive. Beijing wants to move away from dollar hegemony and thus it favours a tripolar monetary system based on the US dollar, the euro and the Chinese Renminbi (RMB). With this in mind, China has continued to diversify its foreign reserves in euros, making it ‘too big to fail’. Finally, the third part focuses on how, by the end of 2011, China switched to a more cautious approach due to the difficulty involved in rescuing the Eurozone. The unwillingness of Europe’s leaders to enter a strategic bargaining process has convinced policymakers in Beijing of the wisdom of keeping a lower profile while making sure the euro’s value remains stable.

Analysis

China’s unequivocal support for the euro

From the early days of EMU, the emergence of the euro as a potential challenger to the US dollar was greeted favourably by China. Chinese policymakers have never been satisfied with dollar unipolarity and thus they welcomed the euro as a counter-balance. With trillions of reserves accumulated over the past decade, diversification of currencies, especially into the euro, has always been one of the Chinese government’s main aims.

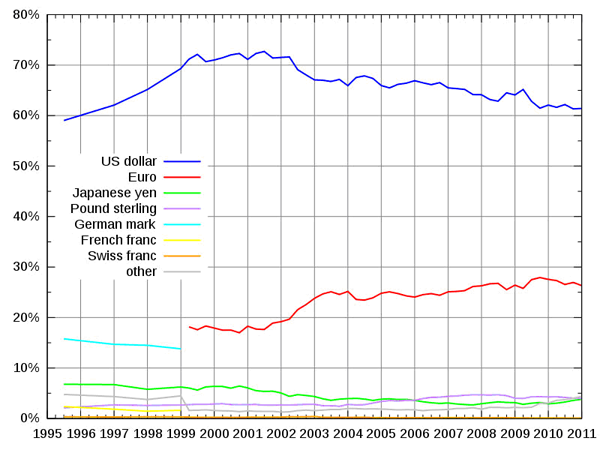

It is common knowledge that the currency distribution of China’s foreign reserves is a state secret. Nonetheless, in an article published in 2010 in the China Securities Journal, unnamed managers from the State Administration of Foreign Exchange (SAFE) disclosed that at the end of the decade (note that this was before the euro crisis) China’s reserves[2] were roughly similar to the global average: 65% were in US dollars, 26% in euros, 5% in Sterling and 3% in Japanese yen (see Figure 1).

Figure 1. Global distribution of foreign exchange reserves, 1995-2011

Source: COFER, IMF.

During the euro crisis open editorials hinting at the possibility of a break-up of EMU from renowned economists such as Krugman and Roubini were a common feature in British and American newspapers. This pessimistic outlook on the euro contrasted with the beliefs of Chinese policymakers and commentators. For an overwhelming majority of the members of the Chinese financial elite interviewed over the past few years for this study, the likelihood of a Eurozone break-up remains remote. They acknowledge that by not having a full-fledged fiscal union there will always be doubts about the project, but in their view the dismemberment of the Eurozone is unlikely.

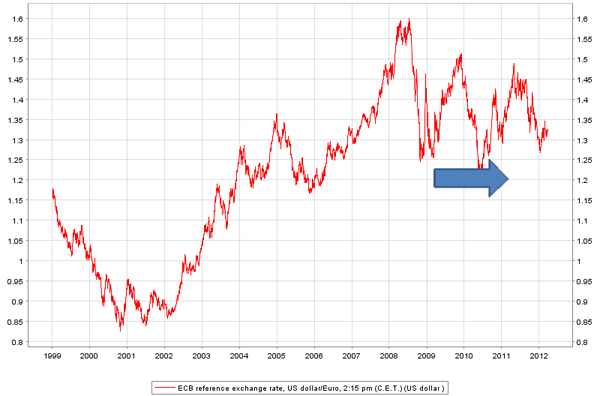

The optimism of China’s policymakers on the euro’s future is reflected in their actions. That the euro was able to maintain its exchange rate value above the US dollar during its greatest existential crisis is partly due to Chinese confidence in the single currency’s long-term consolidation. One of the most critical moments in the euro’s history was 26 May 2010, in the midst of the Greek debt crisis, when a Financial Times report disclosed that China’s SAFE was ‘reviewing its holdings of eurozone debt in the wake of the crisis’.[3] At that moment, the creation of the European Financial Stability Facility (EFSF) had finally been agreed on but there was still much uncertainty in the markets and the euro was still in free fall, approaching the US$1.20 mark from over US$1.50 at the end of 2009 (see Figure 2).

Figure 2. Euro-US dollar exchange rate, 1999 to March 2012

Source: ECB.

On publication of the FT’s report, the single currency plunged another 1.5%, nearing a four-year low against the greenback. Confidence in the euro was vanishing. However, in what can only be interpreted as a coordinated rescue action, the Chinese government stepped in and helped stabilise the euro’s value at a decisive moment. Only hours after the FT report was released, SAFE described it as ‘groundless’ and stressed that as a responsible long-term investor Europe had been and would continue to be one of the major markets for investing China’s exchange reserves.

To dispel any shadow of doubt, that same day Gao Xiqing, Chairman of the China Investment Corporation (CIC), also came out publicly in defence of the single currency and a few days later the President of the National Social Security Fund, Dai Xianglong, also backed it. China’s strategy to help the euro worked: the single currency bottomed out at US$1.1942 on 8 June 2010 and bounced back to over US$1.30 less than a month later (see Figure 2 above).

China’s influence in holding up the European currency was acknowledged by none other than the FX investor George Soros who said after recognising that for some time he had shortened his positions in the single currency that ‘China saved the euro’.[4]

During the rest of 2010 China showed openly and actively its support to the Eurozone periphery in crucial moments. In November 2010, at the time when Ireland had to be bailed out, the Chinese state-owned news agency Xinhua published an editorial titled ‘Euro will not fail’. It said:

‘Contrary to the widespread claim that the eurozone is doomed to break up, the single currency will not fail. […] Despite its shortcomings, which have been exposed by the debt crisis, the euro has brought economic benefits and currency stability to its members. A breakup of the eurozone would be politically unacceptable’.[5]

Again, there is a certain correlation between the euro-dollar exchange rate and Chinese public support. Between 4 November and 29 November 2010, the day the Xinhua editorial was published, the euro plunged from US$1.42 to US$1.31, a considerable fall. Coincidently, after 30 November 2010 the European currency entered a new multi-month rally reaching again a new high of US$1.48 in April 2011 (see Figure 3).

Figure 3. Euro-US dollar exchange rate, 1999 to March 2012

Source: ECB.

This is not to say that the euro’s exchange rate moves depend exclusively on Chinese action. But the strong public support by a player of China’s calibre certainly influences in market perceptions. This interpretation is reinforced by the widespread believe among FX traders that SAFE actively intervenes in the market whenever the euro falls below the US$1.30 mark.[6]

The success of China’s strategy of making the investment community believe that it stands behind the euro was confirmed in February 2011 when the FT’s chief correspondent for international finance, Henny Sender, wrote a piece suggesting that the reason behind the euro’s exchange rate strength vis-à-vis the greenback was that ‘the Chinese have been buying European sovereign debt in a big and –for China– very public way’.[7]

Despite all these reports, and widespread comments in the press that China has increased its holdings of debt from Italy, Spain, Ireland, Portugal and Greece, the truth is that no-one knows for certain how much European debt China holds and whether it has invested mostly in core or peripheral debt. Unlike the US, European countries do not disclose the holders of their debt so they can claim that China is investing in them without proving it, and China can do the same. Thus, we can only estimate Chinese purchases. Nevertheless, after looking at the evidence at hand, it is fair to say that overall China has probably continued its longstanding diversification strategy away from the dollar and into the euro during the crisis.

A number of studies published between 2011 and 2012 by Standard Chartered Bank, Bank of America-Merrill Lynch and Bank of New York Mellon showed that China had effectively diversified substantially between June 2010 and June 2011. While previously 65% of new purchases were dollar-denominated instruments in line with the overall distribution of the accumulated stock, during this period, dollar denominated assets would only account for 54% of total purchases, with the euro being the beneficiary of this shift.

Thus, the data support Chinese Premier Wen Jiabao’s statement in June 2011 during his visit to Europe that ‘China is a long-term investor in Europe’s sovereign debt market’ and that ‘in recent years we have increased by quite a margin our holdings’.[8]

In March 2012 the head of SAFE, Yi Gang, reiterated that China had propped up the European currency by buying debt from financially stressed countries. However, in this same intervention Yi did not explicitly say that China would continue to buy Eurozone peripheral debt. To the contrary, he underlined that henceforth China would rather invest in industrial and strategic assets in Europe so as to ‘avoid internal criticism of bailing out rich Europe’.[9]

This more cautious approach points to a change of strategy by China at the end of 2011 and beginning of 2012, as explained below.

Explaining China’s support for the euro

At this point, however, it is worth explaining why China is confident in the success of the European currency and why it is willing to invest political and financial capital in the project. Five intertwined reasons are here identified.

(1) Diversification of foreign reserves

The first factor to explain why China has been supporting the euro is that China has become over-dependent and overexposed to the US dollar. The greenback’s value has been in structural decline for decades and this is a major worry in Beijing. A US$4 trillion-strong foreign exchange market player with China’s fire capacity has limited choices when it comes to diversifying its assets. It needs a deep, broad and liquid market to allocate its FX investments. The only other currency that can cope with Chinese diversification is the euro, and even so it has its limits. The US$1.60 level reached in 2008 is widely seen in the markets as the upper limit.

(2) Preserving the value of euro-denominated debt

By increasingly diversifying into the single currency, China has also become more concerned about the value of the euros that it already has. As mentioned above, in 2010 sources within SAFE disclosed that approximately 26% of China’s foreign exchange reserves were allocated in euro-denominated instruments. The evidence collected for this study shows that, notwithstanding some ups and downs, it is very likely that, overall, China has maintained its long-term diversification strategy into the euro throughout the crisis, which means that by now the share of its euro holdings needs to be slightly higher, at around 30%. Taking into account that China has US$4 trillion in reserves, this means that its euro holdings are at over US$1 trillion. To put this into context, this is more than the fire power of the European Stability Mechanism (ESM). In other words, the euro is too big to fail for China.

(3) The importance of the European market

China’s calculations are not only focused on maintaining the value of the euro to keep the purchasing power of its national wealth allocated in euro-denominated products. It also needs a relatively strong euro to maintain its export competitiveness in the Eurozone and the EU at large. The Eurozone is China’s second-biggest export market after the US (and the EU the largest), so if the euro depreciates vis-à-vis the RMB, Chinese products will be less in demand. This is an important factor because China is still largely dependent on its export sector to keep unemployment low. Furthermore, the EU market is important for Chinese exports but also for its imports and for acquiring Western know-how in technology and branding. The EU is the main provider of high value-added technology to China. Therefore China has an intrinsic interest in maintaining economic, political and social stability in the Eurozone. Again in this case, the euro is too big to fall and too important to fail for China.

(4) Increasing the political influence in Europe

By supporting the euro in a moment of crisis, the Chinese government has been seeking to augment its political influence in Europe, especially in cash-strapped peripheral countries, and gain the Europeans as allies in international economic disputes. Since the crisis started, for instance, European officials have refrained from publicly criticising the RMB’s under-appreciation. By September 2011, after more than a year supporting the Eurozone periphery, China started to ask openly for some return for its help.

This seems to be a crucial moment in China’s attitude towards the Eurozone crisis. It was the time when China’s leaders believed they could strike a deal with their European counterparts and consequently reinforce the strategic partnership between China and the EU. The offer was made explicit by premier Wen Jiabao when he indicated ‘that the granting to China of Market Economy Status (MES) and/or lifting the EU arms embargo would be regarded favourably by both Chinese leaders and citizens and thus help support China’s bailing out of rich Europe’.[10]

(5) The desire for a tripolar world

Ultimately Chinese policymakers dismiss the idea of a euro break-up because they believe in the construction of a multi-polar world order out of US hegemony. While a G-2 formed by the US and China to govern the world might be a fashionable concept in the US, this is a proposal that does not find great support in Beijing. China feels uncomfortable about wrestling with the mighty US alone: instead, China wants to construct a multipolar world and Europe is seen as an important pole in this new configuration. A triangular balance of power is a synonym for political stability in traditional Chinese culture. Thus, in their ideal scenario of a tripolar world order Chinese policymakers need a strong, united and independent EU with enough strength to help China counterbalance US dominance. The euro is a vivid representation of the European integration project, and therefore its survival needs to be assured.

China scales down its open support for the euro

It appears that by autumn 2011 China’s strategy towards the single currency reached a watershed. Ironically, this coincided with the moment when European policymakers started to openly ask China for financial support. At the end of October 2011, the head of the EFSF, Klaus Regling, flew to Beijing to convince the Chinese authorities to invest in the European rescue fund. The visit was widely reported in the press. Such media attention was counterproductive, however. It only helped to strengthen the voices in China that questioned that developing China should rescue developed Europe.

China’s support for the eurozone would have been easier to justify to its domestic audience if China’s leaders had had something to show in exchange for their financial efforts. However, according to several Chinese participants in this research project, the feeling in Beijing is that Europe has underappreciated China’s help.

First of all, despite promises to review the matter, the Europeans were unwilling to grant China market-economy status. This left former Premier Wen Jiabao frustrated because it was one of his main objectives during his 10-year-long mandate. Secondly, there was the feeling that public opinion in Europe was increasingly hostile to China’s financial clout. Talk about China rescuing the Eurozone periphery only increased the ‘China Threat’ rhetoric.

Overall then, China saw its support for the euro as a strategic move to strengthen its partnership with Europe, while the Europeans continued to see the relationship purely on strictly economic grounds. In this respect, the euro appeared to be too hard to rescue.

Confronted with European unwillingness to enter into a quid-pro-quo deal, policymakers in Beijing decided to change their strategy by taking up the rhetorical argument that China can certainly help, but ultimately it is down to the Europeans to solve their own crisis. Thus, moving away from unsuccessful bilateral help, in 2012 China decided that it was smarter to provide help to the Europeans through the multilateral route of the IMF.

The move aimed to achieve several goals. It avoided the rejection of public opinion in China and Europe. It reinforced China’s demands to increase its voting power in the IMF and indirectly it put pressure on Europe to get its act together because the funds pledged by the BRICS countries are conditional on the Europeans reducing their seats in the executive board of the IMF, as agreed back in 2010.

China discovers the German strategy for the euro

Considering the active support China had offered the Eurozone periphery during the crisis and the close relationship between Berlin and Beijing, its policymakers were eager to discuss with their German counterparts how support could be translated into a strategic alliance between Europe and China. To their surprise, though, Berlin, instead of thanking Beijing for its financial help and entering into a strategic conversation, sent a clear message that its purchases were rather counterproductive.

As several Chinese and European officials confirmed in interviews conducted for this study, at the peak of the crisis Berlin’s response to Chinese purchases of Eurozone peripheral debt was: Sovereign bond spreads are an efficient pressure mechanism to force political leaders in the peripheral countries to undertake the necessary structural reforms to regain competitiveness. It is precisely in this way that Germany, in collaboration with the ECB, was able to force the resignation of Silvio Berlusconi. This level of intra-European brinkmanship puzzled Chinese officials and revealed the complexity of European politics to them.

Overall, Germany’s strategy, as described by Chinese officials, has been to use this crisis to ‘build more Europe’ along federal lines. This has been achieved by forcing reluctant countries to agree to pool further sovereignty under supranational structures. It should be emphasised that Germany has always claimed that monetary union is impossible without political union.[11] Thus, Merkel’s ‘hands-off’ approach has the objective, shared by the ECB, of using market pressure to achieve the fiscal and political union necessary to make the euro a sustainable currency.

Market pressure is used in two steps. First, the market strain forces political leaders to undertake the structural reforms demanded by Berlin and Frankfurt. As the president of the ECB, Mario Draghi, has recognised: ‘high interest rates are the most significant source of pressure for a government resisting reform’.[12]

Secondly, if the efforts are insufficient and pressure continues, these countries are then obliged, as now officially required by the ECB’s Outright Monetary Transactions (OMT) programme, to ask for a rescue package from the European Stability Mechanism (ESM), which means that they will have to give up further sovereignty to Brussels.

The German brinkmanship strategy is not without risk. In fact, China’s worries about the harsh medicine administered by Germany have come up in several of the interviews conducted for this paper. A senior Chinese official disclosed that German officials had told them several times that they should not buy too much debt from these countries in order to maintain the pressure for reforms, but he himself told Merkel in her February 2012 visit that it is important to combine fiscal consolidation and structural reforms with investment, with what China calls ‘development’.

To sum up, from the end of 2011 a number of reasons made China more cautious about openly supporting the Eurozone periphery: the Europeans’ unwillingness to enter into a strategic deal in response to financial support, the public opinion backlash both in China and in Europe and the realisation that Germany, its most trusted partner in Europe, might have its own strategy to solve the crisis.

German influence on Chinese thinking should not be underestimated. The other causes for China’s cautious approach are certainly important, but it is significant that several interviewees with close links to the Chinese leadership recognise that perhaps it was a mistake to intervene so openly in 2010 and 2011 in the Eurozone periphery debt markets and thus undermine Germany’s long-term strategy.

Interestingly, this more low-profile strategy by China seems to have had a certain influence on the markets. In the first half of 2012 Italian and Spanish debt yields started to soar due to the lack of demand from international investors (See Figure 4).

Figure 4. Spanish and Italian 10-year bond yields, January to October 2012

At the same time, in the FX market, from the end of 2011 until July 2012 –when Draghi delivered his game-changing speech about the irreversibility of the single currency– the euro began a steady decline from US$1.45 to US$1.20 (see Figure 5). During the period, the European currency even breached the US$1.30 mark, which, as mentioned, for numerous FX traders is an artificial floor set by SAFE.

Figure 5. Euro-US dollar exchange rate, 1999 to March 2013

Source: ECB.

Again, China’s lack of action during the period might not be the only reason why Italian and Spanish debt yields rose and the euro lost value. This was the period of the ECB’s Long Term Refinancing Operations (LTROS) which pushed the euro down, and when general market sentiment worsened because of the perceived possibility of Grexit. In any case, as mentioned above, the absence of a player like China in the markets has major effects, not least because when it leaves it encourages others to leave too. This, of course, is also applicable when it returns to the market to prop up the euro.

Conclusion: How can China’s longstanding support for the euro be explained? Five reasons have been highlighted: (1) China needed to reduce its over-dependence on the dollar and the euro is the only credible alternative; (2) by maintaining its diversification trend over the years China has now accumulated over US1$ trillion worth of euros; (3) the European market remains crucial for China’s development; (4) China has been eager to use its financial support to strengthen its strategic leverage in Europe; and (5) China favours a multipolar world order in which the EU functions as the third main pole capable of counterbalancing US hegemony. These elements make the euro too big to fail for China’s policymakers.

Nevertheless, this paper has also shown the difficulties China has encountered in converting its financial support for the Eurozone periphery in strategic outcomes. Public opinion both in China and Europe rejects the idea that poor China should bail out rich Europe. Furthermore, European policymakers have been unwilling to enter into any strategic bargaining. Europe has not granted China market-economy status and neither has it lifted its arms embargo, partly because this would upset the US, which remains Europe’s closest strategic partner. Hence, the euro turned out to be too hard to rescue.

For all these reasons, at the end of 2011 Beijing scaled down its support for the Eurozone periphery. Ironically, when the Europeans publicly asked for Chinese financial help, Beijing insisted that it would have to be channelled through the IMF. It was a mistake for the Europeans to ask for financial support from Beijing in such a public manner considering that Chinese policymakers are very careful not to be seen at home as bending to external pressure.

China’s reluctance to help was also due to the fact that the Europeans did not have a united strategy. Chinese policymakers were confronted with contradictory signals. On the one hand, policymakers from the crisis-hit countries would ask them to invest in their debt and thus strengthen their strategic interdependence. On the other hand, German officials would tell them that help was counterproductive and that there was nothing to negotiate in the strategic realm. Confronted with this level of intra-European brinkmanship, it is no wonder that Chinese policymakers decided to step back and let the Europeans solve the crisis by themselves.

This does not mean, however, that China will stop supporting the European currency. A distinction needs to be made between China hoping to use its financial help to increase its strategic leverage in Europe and its desire to diversify into the euro based on economic and broader geopolitical considerations. China, for instance, would be very keen to invest in Eurobonds. Until this level of fiscal and political integration is achieved, though, the most likely scenario is that China will continue its diversification trend while regularly intervening in the market every time the euro falls significantly below the US$1.30 mark.

China’s support is both a blessing and a curse for the Eurozone. While China is a key player in maintaining market confidence in the Eurozone, at this stage a weaker euro would be exactly what the Eurozone periphery needs to rebalance its current-account deficit and repay its debts.

Miguel Otero-Iglesias

Senior Analyst for the European Economy and Emerging Markets, Elcano Royal Institute | @miotei

[1] This ARI is a condensed version of the academic article by M. Otero-Iglesias (2014), ‘The euro for China: too important to fail and too difficult to rescue’, The Pacific Review.

[2] Reuters (2010), ‘China offers rare glimpse into reserves, heavy in dollars’, 3/IX/2010.

[3] Financial Times (2010), ‘China reviews eurozone bold holdings’, 26/V/2010.

[4] Reuters (2010), ‘Soros: China Saved the Euro’, 15/IX/2010.

[5] Xinhua (2010), ‘Euro will not fail’, 29/XI/2010.

[6] M. Casey (2012), ‘China, ECB, odd bedfellows in the euro’s resilience’, Market Watch (WSJ), 9/V/2012; T. Durden (2011), ‘It’s official: China is the “mystery” daily buyer of billions of euros’, Zero Hedge Blog, 26/VI/2011.

[7] H. Sender (2011), ‘China has much to gain from supporting the euro’, Financial Times, 3/II/2011.

[8] Reuters (2011), ‘China to remain long-term investor in Europe’s debt’, 25/VI/2011.

[9] China Daily (2012) ‘Show of confidence in Europe’, 13/III/2012.

[10] N. Casarini (2012), ‘For China, the euro is a safer bet than the dollar’, European Union Institute for Security Studies Analysis Paper, EUISS, Paris, June.

[11] M. Otero-Iglesias (2014), ‘Germany and Political Union in Euro: Nothing moves without France’, Working Paper, nr 8/2014, Elcano Royal Institute, Madrid.

[12] Der Spiegel (2012), ‘We couldn’t just sit back and do nothing’, interview with the ECB president Mario Draghi, 29/X/2012.