Theme: Although the emergence of the US as an unconventional energy power is shifting the global energy balance, its geopolitical consequences for the EU should not be exaggerated and should not distract attention from Europe’s already pressing energy policy agenda.

Summary: The IEA’s World Energy Outlook-WEO 2012 projects a significant geographical shift in hydrocarbon production due to the unconventional hydrocarbon revolution in North America. But neither Middle Eastern, Russian nor North African producers will be pushed to the fringe of the international geopolitical scene. The EU will remain linked to its traditional suppliers of conventional resources, but uncertainties regarding the development of unconventional resources should not put at risk investment on either renewables at home or conventional resources in the European neighbourhood. This paper criticises the excesses involved in reasoning by analogy when dealing with the geopolitics of alternative energy futures: unconventional oil and gas are not necessarily from Mars, and renewables are not essentially from Venus.

Analysis

Introduction

The release of the IEA’s World Energy Outlook-WEO 2012, which projects a significant geographical shift in hydrocarbon production, has been widely echoed by the international media and attracted a lot of attention from policy makers and energy analysts alike. In most analyses, US energy independence and even its emergence as an oil exporter are almost being taken for granted. On this assumption, it is being mechanically argued that US geopolitical interests in the Middle East will almost disappear. ‘Saudi’ America will lead the world’s energy markets, pushing conventional producers to the fringe of the international geopolitical scene;[1] Europe will stand alone in providing for its energy security, increasing European energy vulnerability.

While not denying that the development of unconventional hydrocarbons constitutes a fundamental shift in the geopolitics of energy, this paper will argue, first, that the geopolitical consequences of the US emergence as an unconventional energy power are being exaggerated and, secondly, that interdependence rather than independence will remain the name of the global energy game, especially in Europe. It will then cast a more nuanced view on the prospects for the geopolitical irrelevance of the Middle East, arguing that the region should continue to be a fundamental pivot in the global energy markets, which will continue to be dominated by conventional hydrocarbons in the foreseeable future, and that while US interests in the region may tend to diminish, they are unlikely to end in a strategic retreat. Finally, the paper takes a closer look at the possible impact these developments might have on the EU, arguing that conventional supplies will endure at the core of its energy geopolitics. It also addresses to what extent the coexistence of an unconventional US and a conventional EU poses an asymmetrical energy security risk for the latter.

Given the resonance of some of the IEA’s 2012 WEO messages, the discussion that follows is profusely illustrated with some of its own graphs. They are also compared with the figures provided by the US Energy Information Administration’s 2012 Annual Energy Outlook. Some observers have noted that the IEA is ‘treading a fine line’ by going beyond analysis to normative advice and public advocacy.[2] This is especially true when including geopolitical considerations and orienting the focus of public opinion towards some results rather than others. In this regard, it is important to identify the nuances of the IEA’s own arguments, especially those which have gone most unpublicised.

An Unconventional Power

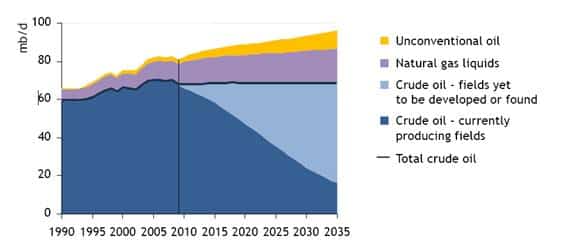

The shale gas revolution has certainly changed the global energy landscape over the past decade, and has been at the centre of most energy geopolitical discussions in the last few years. There have been a plethora of reports dealing with its distinct dimensions, from the geopolitical to the technical, industrial or environmental aspects of the issue. What is relatively new in the recent IEA 2012 WEO is the extension of the shale gas revolution to the domain of unconventional oil (mainly tight oil). The Agency already projected a significant increase in unconventional oil production in its 2010 WEO. Together with new oil field developments and discoveries, unconventional oil would be able to increase global oil production to close to 100 million barrels per day-mb/d (see Figure 1).

Figure 1. Oil production by type, 1990-2035 (million barrels per day-mb/d)

Source: IEA (2010), World Energy Outlook 2010, Paris.

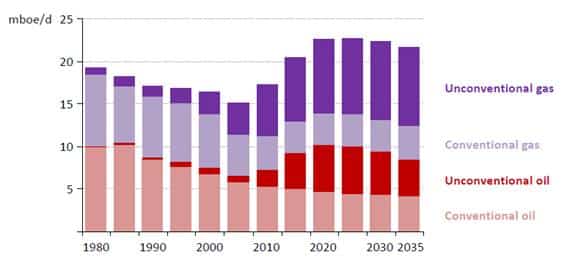

The 2012 WEO reveals that, according to the IEA’s projections, unconventional oil is to become the main contributor to US oil production towards 2020, a decade after unconventional gas surpasses conventional gas production in the country. Figure 2 shows these projections by fuel type. The overall picture is that US oil and gas production is projected to peak around 2020 at some 22-23 million barrels of oil equivalent per day, before slightly declining until 2035. Unconventional gas is the main driver of increased US hydrocarbon production, and will remain stable over the whole projected period. Unconventional oil production is projected to increase quite rapidly to reach its peak around 2020 and then to decline steadily until the end of the forecasted period. By 2035, unconventional hydrocarbons will dominate US production and unconventional oil should account for half its oil production, which should stabilise at around 8 mb/d, down from the 2020s 10 mb/d peak.

Figure 2. US oil and gas production, 1980-2035 (mb/d)

Source: IEA (2012), World Energy Outlook 2012, http://www.worldenergyoutlook.org.

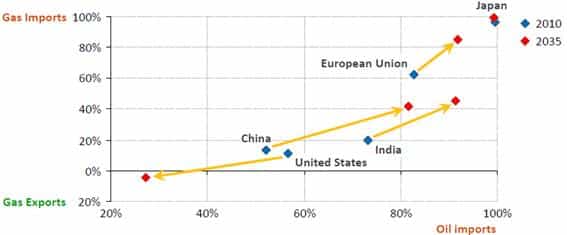

The absolutely novel item in the WEO’s projections (p. 74) is the impact on oil demand from the transport sector due to the new fuel efficiency standards recently approved by the Obama Administration to curb oil consumption. However, this driver of reduced oil dependency has gone relatively unnoticed, to the point that IEA’s Chief Economist, Fatih Birol, has tried to reduce enthusiasm on the drastic production-related geopolitical messages of the report and highlighted the impact of US efficiency measures, as well as the transition from oil to gas in the transport sector.[3] As a result of increased fossil fuel efficiency and unconventional development (including bioenergy), the IEA projects net US oil dependency to be greatly reduced. Figure 3 reproduces the WEO’s projections: US oil dependency falls significantly from almost 60% in 2010 to under 30% in 2035 and the country becomes a small natural gas exporter by 2020 and up to the end of the projected period.

Figure 3. Net oil and gas import dependency in selected countries, 2010-2035 (%)

Source: IEA (2012), World Energy Outlook 2012, http://www.worldenergyoutlook.org.

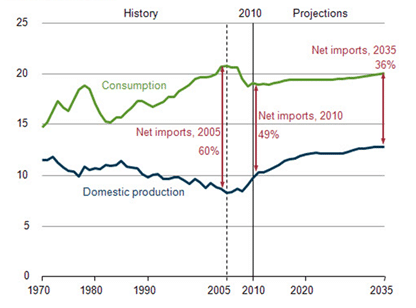

These figures are slightly more optimistic regarding US unconventional production and fuel efficiency trends than those from the US Energy Information Administration (US EIA) itself. In its Annual Energy Outlook 2012, total net imports to the US of petroleum and other liquids are projected to decrease from 49% in 2010 to 36% in 2035 in the reference scenario (Figure 4). It should be highlighted that in a low price scenario, US oil imports would remain at around 50% of consumption in 2035. In general, the IEA baseline projections tend to converge with the US EIA’s more favourable scenarios, but the trend is about the same.

Figure 4. Total US production, consumption and net imports of petroleum and other liquids, 1970-2035 (mb/d)

Source: US Department of Energy, Energy Information Administration, Annual Energy Outlook 2012, http://www.eia.gov/forecasts/aeo.

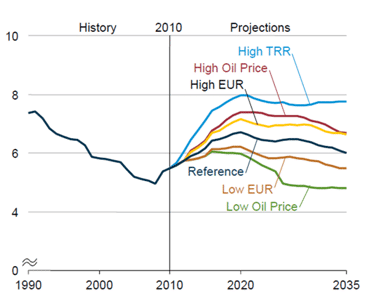

Figure 5 shows how the US EIA’s projections broadly depend on prices and recoverable resources. The reference scenario projects a peak in oil production for 2020, and a gradual decline until 2035 to 6 mb/d, substantially less than the 8 mb/d IEA projection. Given the uncertainties surrounding unconventional resources, low recovery scenarios result in fast peaking and declining oil production, while in most favourable ones oil production reaches a plateau at around 8 mb/d. Oil prices are also decisive: high prices increase US production by 2 mb/d relative to the low price scenarios. Under the most favourable scenario, the US EIA’s projection points to the US producing less than 3 mb/d tight oil by 2035. Even if less optimistic than the IEA’s 4 mb/d, this is an impressive figure, in the same order of magnitude as current world-class producers such as Mexico, Venezuela, Iraq, Kuwait and Nigeria.

Figure 5. Total US crude oil production in six cases, 1990-2035 (mb/d)

TRR = Technically Recoverable Resource; EUR = Estimated Ultimate Recovery.

Source: US Department of Energy, Energy Information Administration, Annual Energy Outlook 2012, http://www.eia.gov/forecasts/aeo.

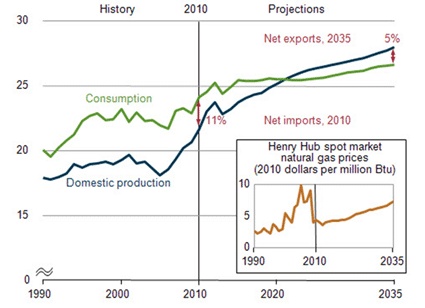

For natural gas, IEA and US EIA projections are much the same, as shown in Figure 6. By 2035 the US should register a 5% net gas export surplus, assuming that the required gas export infrastructures are in place. However, the small box in Figure 6 reflects the true and current significance of the US shale gas revolution: a drastic fall in gas prices that gives the US a competitive edge compared with industrial countries that have not been blessed with unconventional resources, or that remain undecided on what to do with theirs. The 2012 WEO points out that natural gas prices in the US are one-fifth of import prices in Europe and one-eighth of those in Japan, and projects higher gas prices in Europe for the whole period under consideration.

Figure 6. Total US natural gas production, consumption and net imports, 1990-2035 (trillion cubic feet)

Source: US Department of Energy, Energy Information Administration, Annual Energy Outlook 2012, http://www.eia.gov/forecasts/aeo.

Whatever the intensity and the technological resilience with which shale gas and tight oil will finally be exploited in the US, the country is on its way to becoming an unconventional-energy power. Being unconventional means being less dependent on conventional suppliers abroad and more on the technological breakthroughs required to sustain production at plateau levels and avoiding fast declines after 2020. Admittedly, the new pattern of US energy interdependence entails a significant shift in global energy geopolitics, and consequently on world geo-economics. However, this is restructuring US energy interdependence with the rest of the world, rather than leading to energy independence. A much less analysed issue is the challenge to domestic US energy policy to avoid increasing production uncertainty and price volatility as new unconventional supplies with different costs, yields and carbon content reach the market, sacrificing energy diversification at the expense of renewable energies.[4]

While the US economy will remain vulnerable to international oil prices, price spikes will spur local production and partially compensate for the shock. No other industrial country, apart from Canada, benefits to the same extent from this possibility. In other words, interdependence does not imply symmetry: we are all interdependent, but some are more interdependent than others, to put it à la Orwell. In this regard, in the future, oil price shocks will increasingly be more of an asymmetrical shock, impacting relatively more in consumer countries deprived of unconventional resources. North America is reinforced and becomes a net oil exporter when counting on the development of the vast Canadian and Mexican unconventional resources. But this does not necessarily push conventional hydrocarbon producers to the dustbin of global energy geopolitics.

A Conventional Truth

Some figures can help place the relevance of unconventional resources in perspective. According to the 2012 WEO (p. 102, table 3.4) and under the ‘New Policies Scenario’, in 2035 world unconventional oil production should reach 13.2 mb/d (4 mb/d in 2011), compared with 65.4 mb/d for conventional crude oil and 18.2 mb/d for natural gas liquids (68.5 and 12 mb/d, respectively). This is only 13.6% of 2035 total liquids production, but provides most of the additional production, together with natural gas liquids. As explained in the previous section, this is expected to be mainly a North American phenomenon. Regarding natural gas, unconventional gas (mainly shale gas) should rise from 16% to 26% of world production, accounting for close to half of its increase between 2011 and 2035. Half should come from China (30%) and the US (20%) (ibid., p. 141).

These are quite significant figures, mainly because they explain most of the new production capacity. But they should be kept in perspective when compared with the foreseen dominance of conventional resources. Even if unconventional oil and gas are making the US an unconventional (energy) power, the 2012 WEO itself rightly warns that no country is immune to the evolution of the global markets (oil more than gas), and that ‘reducing its oil imports will not insulate the United States from developments in international markets’ (p. 24). The major energy risk to the US is the economic cost of a major disruption in global oil supplies,[5] and the fact is that global oil markets will remain dominated by conventional producers. The figures above show that when adding biofuels, the US may come close to Saudi oil production for some years, even a decade (2020s), before declining. But the current structure of the global oil market will remain dominated by conventional traditional producers through the development of existing fields and new conventional discoveries (including high-cost deep-water fields).

Table 1 shows the current situation. In 2011 Saudi Arabia was the leading oil producer, with over 11 mb/d accounting for 13.2% of world oil production. It was also the leading oil exporter, its 8.3 mb/d making up over 15% of world exports. The total Middle East represents roughly a third of world oil production and exports, and almost half of the world’s proved oil reserves. Even more important for its influence on the global oil market is the fact that it has the world’s only existing spare capacity. Saudi Arabia, together with other smaller Gulf producers, will retain the power to balance (or not) the global oil markets by squeezing or preserving its spare capacity. This will be the only cushion to offset strikes in Nigeria, hurricanes in the Gulf of Mexico, disruptions in Libyan production or the oil embargo on Iran, to name but a few.

Iraq is another variable that can become a game changer in the oil market, as the 2012 WEO highlights. Its projections point to Iraqi oil production rising from 3 mb/d in 2012 to 6 mb/d in 2020 and to over 8 mb/d in 2035. This would mean exports of over 4 mb/d in 2020 and of over 6 mb/d in 2035, up from more than 2 mb/d in 2012. These are ambitious figures that date back to the unfulfilled promises given after the occupatrion of Iraq and which depend on the country’s political evolution. Iraqi exports of 8 mb/d by 2035 would equal US conventional and unconventional oil production.

Figure 7. Oil production and exports, 2011 (thousand barrels daily)

|

Oil production |

Oil exports (production-consumption) |

|||

|

2011 |

Share of total (%) |

2011 |

Share of total (%) |

|

|

US |

7,841 |

8,8 |

-10,994 |

-20,1 |

|

Canada |

3,522 |

4,3 |

1,228 |

2,3 |

|

Mexico |

2,938 |

3,6 |

911 |

1,7 |

|

Total North America |

14,301 |

16,8 |

-8,855 |

-16,2 |

|

Argentina |

607 |

0,8 |

-2 |

0,0 |

|

Brazil |

2,193 |

2,9 |

-460 |

-0,8 |

|

Colombia |

930 |

1,2 |

677 |

1,2 |

|

Ecuador |

509 |

0,7 |

282 |

0,5 |

|

Venezuela |

2,720 |

3,5 |

1,888 |

3,5 |

|

Total S. & Cent. America |

7,381 |

9,5 |

1,140 |

2,1 |

|

Azerbaijan |

931 |

1,1 |

851 |

1,6 |

|

Kazakhstan |

1,841 |

2,1 |

1,628 |

3,0 |

|

Norway |

2,039 |

2,3 |

1,787 |

3,3 |

|

Russian Federation |

10,280 |

12,8 |

7,319 |

13,4 |

|

UK |

1,100 |

1,3 |

-442 |

-0,8 |

|

Total Europe & Eurasia |

17,314 |

21,0 |

-1,610 |

-3,0 |

|

Iran |

4,321 |

5,2 |

2,497 |

4,6 |

|

Iraq |

2,798 |

3,4 |

NA |

NA |

|

Kuwait |

2,865 |

3,5 |

2,427 |

4,4 |

|

Qatar |

1,723 |

1,8 |

1,485 |

2,7 |

|

Saudi Arabia |

11,161 |

13,2 |

8,305 |

15,2 |

|

United Arab Emirates |

3,322 |

3,8 |

2,651 |

4,9 |

|

Total Middle East |

27,690 |

32,6 |

19,614 |

35,9 |

|

Algeria |

1,729 |

1,9 |

1,384 |

2,5 |

|

Angola |

1,746 |

2,1 |

NA |

NA |

|

Egypt |

735 |

0,9 |

26 |

0,0 |

|

Nigeria |

2,457 |

2,9 |

NA |

NA |

|

Total Africa |

8,804 |

10,4 |

5,468 |

10,0 |

|

China |

4,090 |

5,1 |

-5,668 |

-10,4 |

|

India |

858 |

1,0 |

-2,614 |

-4,8 |

|

Indonesia |

942 |

1,1 |

-489 |

-0,9 |

|

Malaysia |

573 |

0,7 |

-35 |

-0,1 |

|

Total Asia Pacific |

8,086 |

9,7 |

-20,215 |

-37,0 |

(1) No data provided for consumption in Iraq, Angola and Nigeria.

(2) 2011 data on Libyan production are not provided for being biased due to the stop in production during that year. In 2010 it represented around 2% of world oil production.

Source: BP Statistical Review of World Energy, June 2012.

In this context, a sudden US strategic neglect of the Gulf region would not seem a plausible option. Especially so in the longer term, when the predominance of Persian Gulf reserves could prove to be more enduring than is currently thought. It is true that US physical oil vulnerability would tend to be reduced. But the US imported only 16.2% of its oil from the Persian Gulf in 2011. The main US supplier is Canada (24.3% of US oil imports), followed by Mexico and Saudi Arabia (10.4% each), Venezuela (8.3%), Nigeria (7.1%) and Russia (5.4%). As seen recently, a reduced reliance on Persian Gulf oil imports did not prevent the US from clearly signalling to Iran that any traffic disruption in the Hormuz Strait would imply military action, or from pushing for the freeing of strategic reserves in the midst of the 2011 Arab revolts.

Middle Eastern energy geopolitics transcend mere oil and gas export flows: Shia-Sunni tensions, competition between regional powers, the Arab-Israeli conflict, the Arab awakening and the geo-economic capabilities of oil exporters (the region accumulates over US$1 trillion in reserves), to name but a few. It is true that the consolidation of the Eastern orientation of the Middle East’s exports introduces new concerns for Asian consumers. Figure 7 shows the 2012 WEO projections for Middle Eastern exports. The shift eastwards is accelerating and by 2035 90% of Middle Eastern oil exports should be directed towards Asia. Meanwhile, Europe should be reducing its imports from the region and the US almost eliminating them.

Figure 8: Middle East oil exports by destination, 2000-2035 (mb/d)

Source: IEA (2012), World Energy Outlook 2012, http://www.worldenergyoutlook.org.

As argued above, this does not necessarily lead to a US retreat from the region and to leaving Asian (and European) consumers to their own devices. But it certainly changes the geopolitical balance in favour of the US when bargaining with its Asian and European counterparts on how to provide energy security as a global public good. Both regions will have to start thinking strategically on how to increase their contribution to global energy security, but the fact is that the US is the best option for providing it and will remain so in years to come.

Figure 9. Estimated shale gas technically recoverable resources for selected basins, compared with existing reported reserves, production and consumption during 2009

|

2009 Natural Gas Market |

Proved Natural Gas Reserves |

Technically Recoverable Shale Gas Resources |

||||

|

Production |

Consumption |

Imports |

||||

|

Europe |

||||||

|

France |

0.03 |

1.73 |

98% |

0.2 |

180 |

|

|

Netherlands |

2.79 |

1.72 |

(62%) |

49.0 |

17 |

|

|

Norway |

3.65 |

0.16 |

(2,156%) |

72.0 |

83 |

|

|

UK |

2.09 |

3.11 |

33% |

9.0 |

20 |

|

|

Denmark |

0.30 |

0.16 |

(91%) |

2.1 |

23 |

|

|

Poland |

0.21 |

0.58 |

64% |

5.8 |

187 |

|

|

North America |

||||||

|

US |

20.6 |

22.8 |

10% |

272.5 |

862 |

|

|

Canada |

5.63 |

3.01 |

(87%) |

62.0 |

388 |

|

|

Mexico |

1.77 |

2.15 |

18% |

12.0 |

681 |

|

|

Asia |

||||||

|

China |

2.93 |

3.08 |

5% |

107.0 |

1,275 |

|

|

India |

1.43 |

1.87 |

24% |

37.9 |

63 |

|

|

Pakistan |

1.36 |

1.36 |

– |

29.7 |

51 |

|

|

Australia |

1.67 |

1.09 |

(52%) |

110.0 |

396 |

|

|

Africa |

||||||

|

South Africa |

0.07 |

0.19 |

63% |

– |

485 |

|

|

Libya |

0.56 |

0.21 |

(165%) |

54.7 |

290 |

|

|

Algeria |

2.88 |

1.02 |

(183%) |

159.0 |

231 |

|

|

South America |

||||||

|

Venezuela |

0.65 |

0.71 |

9% |

178.9 |

11 |

|

|

Argentina |

1,46 |

1.52 |

4% |

13.4 |

774 |

|

|

Brazil |

0.36 |

0.66 |

45% |

12.9 |

226 |

|

|

Chile |

0.05 |

0.10 |

52% |

3.5 |

64 |

|

|

Bolivia |

0.45 |

0.10 |

(346%) |

26.5 |

48 |

|

Source: UE EIA (2011), World Shale Gas Resources: An Initial Assessment of 14 Regions Outside the United States, http://www.eia.gov/analysis/studies/worldshalegas.

These trends are more dramatic in natural gas due to the shale revolution. To what extent tight oil can replicate the success story of shale gas remains an open question. But there is no doubt that shale gas has changed the gas market’s dynamics, although its impact has not been so dramatic outside North America. Figure 9 shows the production, consumption and trade data for conventional gas, and compares its proved reserves with technically recoverable shale gas resources. A few countries have very significant shale gas reserves: China, the US, Argentina, Mexico, South Africa, Canada and Australia; other countries remain on a second tier, like Libya, Algeria, Brazil, Poland, France, Norway and Chile.

The question is that only the US (and Canada) are significant producers: the shale gas revolution has not spread much outside North America, due to social opposition, lack of regulation, absence of technological capabilities and high investment requirements. Regarding Russia, the IEA does not expect the country to replicate the US unconventional success: exploration has been limited and not that promising, resources are dispersed and huge exploration and investment efforts are required.[6] However, it will remain the EU’s main gas supplier in the foreseeable future. By contrast, Norway and Algeria, the EU’s second- and third-largest gas suppliers, have significant unconventional resources. Norway’s Statoil is among the most important players in the shale gas revolution, but interestingly enough its main fields are in the US, not in Norway.

North Africa has attracted the attention of major international energy companies. Algeria’s Sonatrach has signed a cooperation agreement with Eni to develop its unconventional gas resources and is in advanced talks with ExxonMobil and Royal Dutch Shell over shale gas exploration. Middle Eastern companies are also interested in the region: Dana Gas (UAE), the Middle East’s leading private gas company, is studying shale gas opportunities in Algeria and Libya. Other Middle Eastern countries have also shown their interest in developing unconventional gas, and there is the belief among energy analysts that the region has huge undiscovered shale gas resources. There are doubts about the potential in the region given current extraction technologies: water is needed in fracking, but the amount needed has been greatly reduced over the last five years. Governments such as Algeria’s are celebrating that they have shale resources well above international estimates. Jordan, which has the world’s fourth-largest oil shale reserves, intends to reduce its oil and gas dependency by developing them.

Besides technological requirements, that can evolve with technology, the main restrictive factor in the region for both conventional and unconventional continues to be the unattractive fiscal and investment conditions. Furthermore, without denying its shale potential in the long run, the most sensible strategy for Algeria and Libya would be to continue to develop their conventional resources for the years to come. As with Russia’s dominance in Northern and Eastern Europe, North African producers enjoy the benefits of geographical proximity to the South European markets and a flexible export infrastructure. Their position can be weakened in negotiating gas prices, but their comparative advantages will only be challenged in a relative way and will continue to be based upon conventional resources.

The Shifting European Energy Landscape

While not as dramatic as portrayed by some analysts, the unconventional power of the US poses new challenges to an already troubled European energy strategy. Shale gas fans regret the lack of European enthusiasm and the delay in conducting exploratory research and in laying the regulatory foundations for its development. Earlier over-optimistic estimations in countries such as Poland have raised the question of the uncertainty over reserves, which is prevalent in Eastern Europe due to a lack of historical drilling data. Some authors have warned about the risks of the shale gas revolution not delivering on its promises in the US, especially in Europe, and of inhibiting investment in the development of both conventional gas resources and renewables.[7]

According to a recent European study, shale gas would impact global gas markets in a significant way only under strongly optimistic assumptions about its production costs and reserves. Under the most favourable scenario it will not make Europe self-sufficient in natural gas, but might replace declining conventional production and keep import dependence at around 60%, which is a significant contribution.[8]

Shale gas developments affect natural gas producers to a greater extent than unconventional oil does oil producers. As said, oil is traded in a fungible, global market, while gas markets are mostly regional in scope and are far more rigid due to the prevalence of oil-indexed, long-term contracts. It is true that LNG shipments are globalising natural gas markets, and that some gradual convergence in prices is expected across regions, as stated by the 2012 WEO. But for the EU, conventional gas producers will continue to dominate the whole gas picture, because indigenous production faces high uncertainties, trans-regional shale gas flows will remain limited and the market will continue to rely on long-term contracts.

The US can export LNG in the future, but there will be increasing pressure from domestic industries that benefit from cheap gas to raise their competitiveness in the global markets. And while it is possible for Europe to start to import US gas in the coming years, the imports will probably be limited in both quantity and geographical scope. Perhaps the UK and other Atlantic LNG importers might benefit, although price convergence would be slower than expected. Regarding oil, the US will certainly increase its exports of refined products, although they will probably continue to be mostly directed towards Latin America and to a very limited extent to Europe.

On the whole, and notwithstanding the significant changes unconventional oil and gas resources can introduce in the global energy system, without abrupt regulatory and social acceptance breakthroughs, conventional (imported) hydrocarbons will remain the main driver of the EU’s energy geopolitics. Europe stays out of the scene with its failure to decide whether unconventional hydrocarbon resources deserve the chance of being developed and under which environmental and market regulations. Dreams of European immunity to on shale gas are also rightly nuanced by the 2012 WEO, which highlights how low-priced natural gas is reducing coal use in the US, freeing up coal for export to Europe, thereby displacing gas and renewables in the continent. This is the kind of shift that the EU should absolutely avoid.

It is true that shale competition and LNG trade growth are expected to reduce the market power of conventional producers in the EU markets[9]. This is already a matter of concern for Russian, Norwegian and Algerian producers, the EU’s main natural gas suppliers. There is growing evidence that pressure on Gazprom to move away from oil indexation in response to new market fundamentals has led to more flexible contracting possibilities. Unconventional gas adds to the new export capacities developed by the Persian Gulf producers, mainly Qatar, and to the eventual opening of new gas corridors from Central Asia. But European policy-makers should not be comforted by the challenges their suppliers are facing. If the unconventional revolution, especially regarding shale gas, fails to deliver new supplies while inhibiting investment in conventional production and related infrastructures, Europe could find itself in a much more worrying situation than any asymmetrical shock produced by the US neglect of the Middle East.

Instead of incubating geopolitical paranoias, Europe’s leaders should start to make informed decisions. Besides the shale gas issue, there are too many files piling up in the European energy security policy desk: the fulfilment of a truly interconnected single energy market, the achievement of a coherent external energy policy, the viability of the deployment of increased renewables, the diversification towards economically optimal energy corridors from North Africa and the pooling of existing Member States’ LNG and gas storage capacities, to list a few.

What is interesting in the emerging energy interdependence pattern is that it is biased towards the US unconventional energy power, while the alternative renewable low-carbon vision promoted by the European Commission looks increasingly unattractive to strategic European thinking. Besides facing budgetary, regulatory, financing and industrial challenges (subsidies, foreign competition and even dumping, lack of finance), a renewables-based energy mix seems too much a soft energy power. In spite of 2012 WEO projections indicating that by 2035 renewables approach coal as the primary source of global electricity, its appeal is fading in an energy world dominated by the hard narrative of hydrocarbon resources, conventional or unconventional. When dealing with alternative energy futures, unconventional oil and gas are from Mars, while renewables are from Venus, to put it in Robert Kagan’s terms. This might not constitute a rigorous argument, but dismissing it will fail to recognise that such a narrative increasingly impregnates current thinking on energy geopolitics.

Conclusion: This paper recognises that the development of unconventional hydrocarbon production constitutes a fundamental shift in the geopolitics of energy. However, it argues that the geopolitical consequences of the US becoming an unconventional energy power are at risk of being exaggerated, and that the US is prone to a new pattern of energy interdependence rather than independence. The Middle East will remain a fundamental energy player, and global energy markets and geopolitics will continue to be dominated by conventional hydrocarbons and traditional energy players. It is true that US preferences for providing energy security abroad can tend to diminish, but this is unlikely to result in a strategic retreat in key regions like the Middle East. European policy-makers should not be comforted by the hope that the unconventional revolution will reduce their suppliers’ market power. In any case, conventional supplies will endure at the core of the EU’s energy geopolitics.

Instead of being distracted by fears of asymmetrical energy shocks due to the eventual US neglect of the Middle East, or any other new great geo-strategic threat, the EU should concentrate on addressing the significant energy challenges that are piling up on its agenda. This includes defining its stance over the exploitation of unconventional resources in Europe, but not at the expense of introducing additional uncertainties on the investment on renewables in the EU, or for conventional resources in its neighbourhood. Energy geopolitical balances are shifting, but whether the EU should shift towards a more conventional energy mix (including most-conventional coal) or towards alternative unconventional sources like renewables will be a European decision. It would be advisable that such a crucial decision not be taken by default or for the sake of frivolous geopolitical discourse.

Gonzalo Escribano

Director of the Energy Programme at the Elcano Royal Institute

[1] ‘Saudi America. The US will be the world’s leading energy producer, if we allow it’, The Wall Street Journal, 12/XI/2012.

[2] Karel Beckman, ‘The fine line treaded by the IEA’, European Energy Review, 19/XI/2012.

[3] European Energy Review (2012), ‘Interview with Fatih Birol’, 19/XI/2012, http://www.europeanenergyreview.eu.[4] David Burwell & Deborah Gordon (2012), ‘Managing the Unconventional Oil and Gas Bonanza’,

Carnegie Endowment for International Peace, 29/X/2012, http://carnegieendowment.org/globalten/?fa=50162

[5] Keith Crane, Andreas Goldthau, Michael Toman, Thomas Light, Stuart E. Johnson, Alireza Nader, Angel Rabasa & Harun Dogo (2009), ‘Imported Oil and US National Security’, RAND, http://www.rand.org/content/dam/rand/pubs/monographs/2009/RAND_MG838.pdf.[6] Platts: “IEA doubts Russia can replicate US unconventional oil, gas success”, 12/X/2012.

[7] Paul Stevens (2010): ‘The “Shale Gas Revolution”: Hype and Reality’, Chatham House Report, September, http://www.chathamhouse.org/sites/default/files/public/Research/Energy,%20Environment%20and%20Development/r_0910stevens.pdf; Paul Stevens (2012), ‘The “Shale Gas Revolution”: Developments and Changes”, Chatham House Briefing Paper, August, http://www.chathamhouse.org/publications/papers/view/185311.

[8] Institute for Energy and Transport (2012), Unconventional Gas: Potential Energy Market Impacts in the European Union. European Commission, Joint Research Centre, Petten, http://ec.europa.eu/dgs/jrc/downloads/jrc_report_2012_09_unconventional_gas.pdf.

[9] Stratfor, Natural Gas Competition, Part 1: Qatar and Russia in the UK, 3/XII/2012.